How Personal Loans Affect Your Credit Score

A personal loan affects your credit score at three distinct stages: the application (hard inquiry, typically –5 to –10 FICO points), the new account opening

Last Updated: April 2026

SoFi (Social Finance, Inc.) has emerged as one of the most popular online personal loan lenders in the United States, serving over 4 million customers across multiple financial products. Founded in 2011, SoFi began as a student loan refinancing platform and has since expanded to offer personal loans, mortgages, investing services, and savings accounts. The company’s approach combines competitive interest rates with member-exclusive benefits that set it apart from traditional banks and other online lenders.

SoFi personal loans are unsecured, meaning borrowers don’t need to pledge collateral to secure financing. The company uses a proprietary algorithm to assess creditworthiness, considering not just credit scores but also employment history, income stability, and overall financial profile. This holistic approach has made SoFi accessible to borrowers who might not qualify elsewhere, though the company still maintains relatively strict credit requirements compared to some competitors.

The lender distinguishes itself through member-centric products and services. Beyond traditional lending, SoFi provides career coaching, financial planning consultations, and unemployment protection to qualifying borrowers. These value-added services appeal to younger professionals and financially-conscious consumers who view SoFi as more than just a lender but as a comprehensive financial wellness partner.

SoFi offers a full application preview that doesn’t affect your credit score until you formally apply. Use this feature to compare loan offers and terms before committing to a hard credit inquiry.

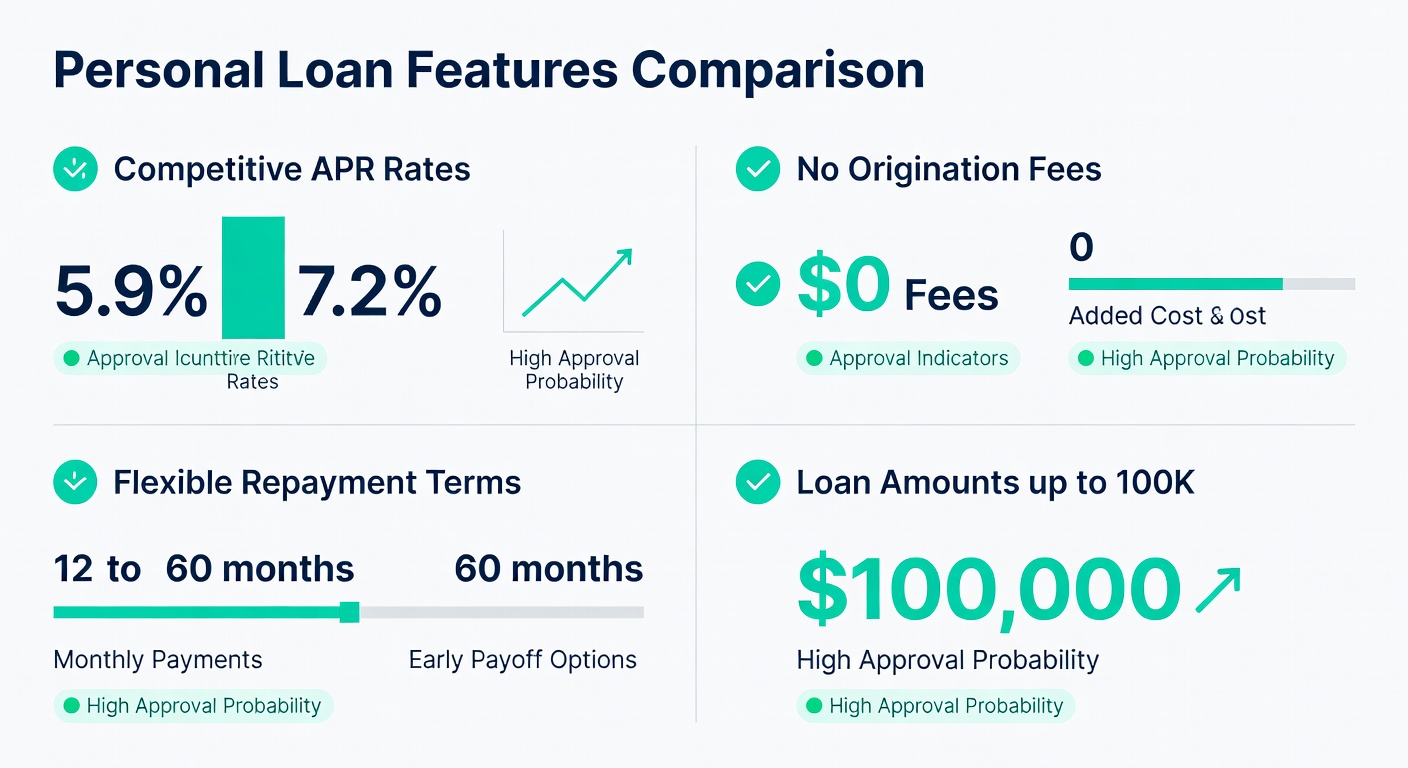

SoFi personal loans feature competitive rates that vary based on credit profile, loan amount, and repayment term. Current APR ranges from 8.99% to 25.81%, with the best rates reserved for borrowers with excellent credit scores (750+), stable employment, and lower debt-to-income ratios. The company updates its pricing regularly based on market conditions and individual creditworthiness assessp.

Loan amounts range from a minimum of $5,000 to a maximum of $100,000, allowing borrowers flexibility in matching their financing needs. Repayment terms span 24 to 84 months, meaning you can structure a loan that fits both your budget and long-term financial goals. Shorter terms (24–36 months) result in higher monthly payments but lower total interest costs, while longer terms (60–84 months) spread payments over more time but increase total interest paid.

| Feature | SoFi Details |

|---|---|

| APR Range | 8.99% – 25.81% |

| Loan Amount | $5,000 – $100,000 |

| Repayment Terms | 24 – 84 months |

| Origination Fee | None (0%) |

| Prepayment Penalty | None |

| Late Payment Fee | Up to $15 |

| Funding Time | 1 business day |

| Minimum Credit Score | ~680 (good credit) |

| Max Debt-to-Income | 50% |

One of SoFi’s standout features is the complete absence of origination fees and prepayment penalties. Many traditional lenders charge origination fees ranging from 1% to 8% of the loan amount, which can add thousands of dollars to your borrowing costs. By eliminating these upfront charges, SoFi makes the loan more affordable from day one. Similarly, prepayment penalties—fees charged when you pay off your loan early—don’t exist with SoFi, giving you complete flexibility to accelerate repayment without financial consequences.

SoFi charges a late payment fee of up to $15 if you miss a payment. This is notably lower than many competitors, which can charge $25–$35 in late fees. However, the best strategy is always to make payments on time, as missed payments damage your credit score regardless of fee amounts.

Enroll in automatic payments to receive a 0.25% APR discount. On a $25,000 loan at 12% APR, this discount saves you approximately $62 annually in interest charges. Every 0.25% reduction compounds to meaningful savings over the loan term.

LightStream, a subsidiary of Truist Bank, is another popular online personal loan provider that often attracts comparison shopping from SoFi prospects. Both lenders serve borrowers with good-to-excellent credit and offer online applications with fast funding. However, they serve different borrower profiles and prioritize different product advantages.

LightStream’s primary competitive advantage is its lowest starting APR: 6.49% for the most creditworthy borrowers. This is 2.5 percentage points lower than SoFi’s 8.99% starting rate. For a $50,000 loan with a 60-month term, this difference translates to nearly $3,000 in additional interest costs with SoFi. LightStream also offers same-day funding in most cases, compared to SoFi’s standard 1-business-day funding. For borrowers focused purely on rate shopping and speed, LightStream may edge ahead.

SoFi counters with two major advantages: comprehensive member benefits and unemployment protection. SoFi’s ecosystem includes career coaching (job interview prep, resume reviews), financial planning consultations, and the Unemployment Protection Plan, which covers up to 6 months of loan payments if you lose your job involuntarily. LightStream offers none of these ancillary services. For borrowers valuing holistic financial wellness and risk mitigation, SoFi’s broader value proposition justifies higher rates.

| Feature | SoFi | LightStream |

|---|---|---|

| Starting APR | 8.99% | 6.49% |

| Max Loan Amount | $100,000 | $100,000 |

| Origination Fee | None | None |

| Prepayment Penalty | None | None |

| Funding Time | 1 business day | Same day (most) |

| Unemployment Protection | Yes (up to 6 mo.) | No |

| Career Coaching | Yes | No |

| Financial Planning | Yes | No |

| Minimum Credit Score | ~680 | 700+ |

LightStream also maintains a slightly higher minimum credit score requirement (700+), whereas SoFi will consider borrowers around 680. If your credit is in the 680–700 range, SoFi may be your only option between these two lenders.

The choice between SoFi and LightStream ultimately depends on your priorities. If you’re rate-sensitive and need funds urgently, LightStream’s 6.49% starting rate and same-day funding may justify the trade-off. If you value holistic financial support, unemployment safety net, and career advancement services, SoFi’s ecosystem provides broader value despite higher rates.

SoFi’s application process is designed to be user-friendly and transparent. Borrowers can apply online in minutes using a mobile app or web browser. The application collects standard information: full name, address, employment details, income, existing debts, and Social Security number for credit verification.

After submitting your application, SoFi provides a preliminary decision within minutes. This initial decision is based on a soft credit inquiry, meaning it doesn’t appear on your credit report and doesn’t affect your credit score. You’ll receive loan term options with corresponding interest rates based on your creditworthiness. This stage allows you to review offers without commitment.

Once you select a loan offer, SoFi proceeds with a hard credit pull, which does appear on your credit report. This step finalizes your rate and terms. If you proceed to formal approval, SoFi verifies employment and income documentation. Most applicants provide recent pay stubs, tax returns, or bank statements to confirm financial stability.

The entire approval process typically takes 1–2 business days from formal application to funding. SoFi transfers funds directly to your bank account, usually within 1 business day of approval. Funding weekends and holidays may extend this timeline slightly.

SoFi’s underwriting requirements include a minimum credit score around 680, though in practice most approved borrowers score 700 or higher. The company prefers debt-to-income ratios below 50%, meaning your total monthly debt payments shouldn’t exceed 50% of gross monthly income. You must be a U.S. citizen or permanent resident, at least 18 years old, and have a valid bank account for direct deposit.

SoFi’s member ecosystem extends far beyond personal loans. All borrowers gain access to career coaching services, including resume reviews, interview preparation, and professional networking guidance. This benefit is particularly valuable for young professionals navigating early career transitions or mid-career job changes. The coaching is provided by qualified career counselors and available through SoFi’s app.

Financial planning consultations are another standout member benefit. SoFi provides access to financial planners who help you map out retirement goals, investment strategies, and overall financial planning. These consultations are typically free for personal loan borrowers, whereas similar services at traditional financial advisory firms charge hundreds of dollars per hour.

The Unemployment Protection Plan is SoFi’s most distinctive benefit. If you lose your job involuntarily (not due to resignation, misconduct, or cause), SoFi covers up to 6 months of loan payments (maximum $25,000 total). This safety net means you won’t default on your loan if unexpected job loss occurs. The protection applies automatically to eligible borrowers at no additional cost.

Additionally, SoFi members receive a 0.25% APR discount for enrolling in automatic payments. On a $30,000 loan at 12% APR, this discount saves approximately $75 annually. Larger loans see proportionally larger savings.

SoFi also offers an online platform for cash management (FDIC-insured savings), investing, and credit monitoring. While these are separate products, members enjoy integrated access and streamlined account management across all SoFi products.

SoFi is ideal for borrowers with good-to-excellent credit (680+) who want a large personal loan ($25,000–$100,000) without origination fees. If you value member services like career coaching and financial planning, SoFi’s comprehensive ecosystem is hard to match. Borrowers concerned about job loss should particularly consider SoFi’s unemployment protection benefit.

SoFi works well for debt consolidation, home improvements, major purchases, and life events requiring substantial financing. The absence of prepayment penalties means you can pay extra toward principal whenever your financial situation improves, accelerating loan payoff without penalties.

However, SoFi may not be the best fit if you have fair or poor credit (below 680). The company’s strict underwriting means low-credit borrowers will face rejection or significantly higher rates. If your primary goal is securing the absolute lowest interest rate, LightStream or other rate-focused lenders might edge SoFi out.

SoFi is also not ideal if you need same-day funding, as the standard timeline is 1 business day. LightStream’s same-day funding option serves time-sensitive borrowers better. If you require a very small loan (under $5,000), SoFi’s $5,000 minimum doesn’t work; you’d need to explore smaller lenders or credit unions.

Borrowers with significant existing debt relative to income (DTI above 50%) will likely face approval challenges, as SoFi caps acceptable debt-to-income ratios at 50%. If your current debts are already pushing this threshold, you’ll need to reduce existing obligations before applying.

SoFi is an excellent personal loan choice for borrowers with good credit (680+) and substantial financing needs ($5,000–$100,000). The lender stands out through its combination of zero origination fees, zero prepayment penalties, competitive APR rates (8.99%–25.81%), and comprehensive member benefits. Unlike traditional banks, SoFi provides access to career coaching, financial planning sessions, and unemployment protection at no extra cost to borrowers.

The company’s strength lies in its holistic approach to personal finance. SoFi treats borrowers as members of a financial wellness community rather than transaction-focused customers. Fast approval (1–2 business days) and quick funding (usually 1 business day) mean you can access needed capital quickly. Whether SoFi is “good” for your situation depends on your credit score, loan amount needs, and whether you value ancillary financial services alongside competitive rates.

SoFi and LightStream serve similar borrower profiles (good-to-excellent credit) but prioritize different advantages. LightStream’s primary edge is its lowest starting APR of 6.49%, which is 2.5 percentage points lower than SoFi’s 8.99% starting rate. On a $50,000 60-month loan, this difference equals nearly $3,000 in additional interest with SoFi. LightStream also typically offers same-day funding, whereas SoFi standard funding is 1 business day.

SoFi counters with substantial benefits LightStream doesn’t offer: career coaching, financial planning consultations, and unemployment protection covering up to 6 months of payments if you lose your job involuntarily. For pure rate shopping and speed, LightStream wins. For holistic financial wellness and job loss protection, SoFi’s broader value proposition justifies slightly higher rates. Choose SoFi if you want member benefits and peace of mind; choose LightStream if you prioritize the lowest possible rate and fastest funding.

SoFi’s minimum credit score requirement is approximately 680, which falls into the “good credit” category. However, approval odds and interest rates improve significantly with scores above 700. Borrowers with excellent credit (750+) qualify for SoFi’s lowest rates, currently starting at 8.99% APR.

If your credit is below 680, SoFi will likely deny your application. Before applying, check your credit report for errors and consider building credit by paying down existing debts and maintaining on-time payment history. Many borrowers in the 650–680 range can reach SoFi’s threshold within 3–6 months of responsible credit management. SoFi’s prequalification process gives you an initial assessment without affecting your credit score, so you can determine eligibility before committing to a hard inquiry.

No, SoFi charges zero origination fees on all personal loans. Origination fees are upfront charges lenders deduct from your loan proceeds or add to your total loan balance, typically ranging from 1% to 8% depending on the lender. A $25,000 personal loan with a 3% origination fee would cost $750 in upfront charges. SoFi’s elimination of these fees saves thousands of dollars on larger loans.

This fee structure makes SoFi particularly attractive compared to traditional bank personal loans, which often charge 2%–5% origination fees. SoFi also charges no prepayment penalties, meaning you can pay extra toward principal or pay off the loan early without financial consequences. The combination of zero origination fees and zero prepayment penalties provides flexibility and savings other lenders don’t offer.

SoFi’s standard funding timeline is 1 business day after approval. Once you submit your formal application and receive conditional approval, SoFi verifies employment and income documentation (typically within hours). After verification, funds are transferred directly to your linked bank account, usually arriving within 1 business day. In many cases, funding occurs on the same day as application if you apply early in the business day.

Weekends and federal holidays may extend this timeline slightly, as the Federal Reserve doesn’t process transfers on non-business days. If you apply on a Friday afternoon, funding may not arrive until Tuesday morning, accounting for the weekend gap. For borrowers needing funds the same day, LightStream offers same-day funding in most cases, though SoFi’s 1-business-day standard is faster than many traditional banks (typically 3–5 days).

Yes, debt consolidation is one of SoFi’s primary use cases. SoFi personal loans are unsecured and flexible, meaning you can use the funds to pay off credit cards, medical bills, personal loans, or other debts. Many borrowers use SoFi consolidation loans to combine multiple high-interest credit card balances into a single, lower-interest personal loan, reducing overall interest costs and simplifying payments.

The math works especially well if you’re consolidating credit card debt (typically 18%–25% APR) into a SoFi personal loan (8.99%–25.81% APR depending on credit). If your credit score qualifies for SoFi’s lower rates (8.99%–12%), consolidation provides substantial savings. Even at SoFi’s higher rates (18%–25%), consolidation still improves your situation if you’re currently paying 20%+ on credit cards. After paying off debt with your SoFi loan, avoid accumulating new credit card balances to truly benefit from the consolidation strategy.

Yes, SoFi offers a 0.25% APR discount when you enroll in automatic payments. While this might seem modest, it compounds to meaningful savings over your loan term. On a $25,000 loan at 12% APR with a 60-month term, this 0.25% discount saves approximately $62 in interest. On a larger $75,000 loan, the savings approach $190 over the same timeframe.

Enrolling in autopay is straightforward through SoFi’s app or online portal, and payments are typically deducted on your loan’s due date each month. This approach eliminates the risk of missed payments (which damage your credit score and trigger late fees), automates your financial obligations, and rewards you with lower interest costs. If you have stable income and a reliable bank account, autopay enrollment is a simple way to reduce your borrowing costs at no additional effort.

SoFi’s Unemployment Protection Plan covers up to 6 months of loan payments (maximum $25,000 total) if you lose your job involuntarily. This benefit is particularly valuable during economic downturns or industry disruptions. To qualify, your job loss must be due to circumstances beyond your control (layoffs, company closure, etc.), not resignation or termination for cause.

The protection process is straightforward: notify SoFi of your job loss, provide documentation (severance letter, unemployment benefits notification, etc.), and SoFi covers your scheduled payments while you search for new employment. This safety net prevents your loan from going into default if temporary income loss occurs. Few personal loan lenders offer this benefit, making it a significant SoFi advantage for borrowers concerned about employment volatility or working in cyclical industries.

A personal loan affects your credit score at three distinct stages: the application (hard inquiry, typically –5 to –10 FICO points), the new account opening

The most common personal loan fee is the origination fee, which ranges from 1% to 10% of your loan amount and gets deducted before you

A personal loan is the cheaper choice for borrowing $3,000 or more when you need longer than 60 days to repay — the average personal

You can prequalify for a personal loan in under five minutes at most online lenders — SoFi, Upstart, Prosper, Best Egg, and Upgrade all let

Most personal loan lenders approve borrowers with a debt-to-income ratio (DTI) under 50%, though the best rates and terms go to applicants below 36%. SoFi,

The prime rate forecast for 2026 is one of the most closely watched financial data points of the year — and for good reason. Every